Liquidnet at TradeTech 2026

21 - 23 April 2026

RAI Amsterdam

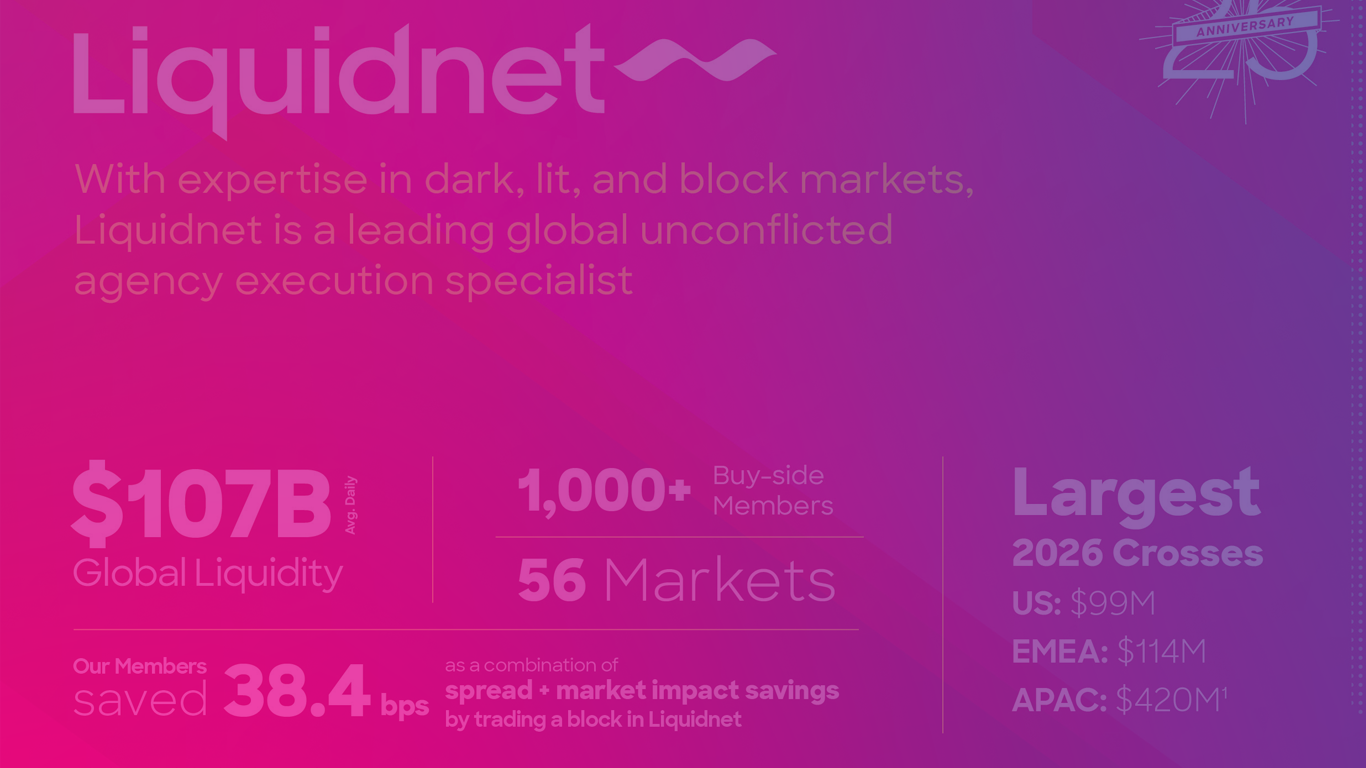

Since its founding in 1999, Liquidnet has been on quite a journey, playing a key role in the trading technology revolution, growing its global network, and being consistently recognized as a leader and trailblazer in financial technology innovation.

From that foundation, we have grown into a full-service global agency execution specialist offering a broad array of trading and execution services.

This year, you’ll find us at booth 102 where you can meet the team and play a game of foosball. Join us there for a cheeky cocktail and a piece of our 25th birthday cake on Wednesday April 22 from 3.00pm.

Meet the team

Live from Trade Tech

Prep for your next session

Stay tuned here during the event while we provide impactful insights to help you make the most of select panels during the day.

Gareth Exton - Head of Execution and Quantitative Services (EQS), EMEA

The day is getting started here at TradeTech, with early discussions centred on unlocking capital and liquidity, timely themes as Europe's market structure continues to evolve.

In European equities, that evolution has increasingly taken the form of fragmentation. What was once a well-marked motorway, now resembles a complex network of venues, protocols and liquidity types. Ahead of the panel, "Navigating fragmented market structure", here's a brief preview of what's likely to be discussed.

What's going on

Equity trading in Europe is increasingly dispersed across a wide range of venues and models. The lit order book no longer sits at the centre of the market as it once did, with bilateral trading, systematic internalisers (SI), periodic auctions, and direct dealer streams taking a growing share of activity. There's even talk of equities adopting FX-style "request-for-stream" interaction. Whether that's evolution or revolution is open to debate, but the direction of travel is clear: more bespoke, less broadcast.

At the same time, this shift is challenging long‑held assumptions around transparency and price formation. As more volume trades off-exchange, the ability of lit markets alone to reflect the full pricing picture is under pressure. While initiatives such as a consolidated tape may eventually improve visibility, for now the picture remains incomplete. For those of us focused on execution quality, that presents a real challenge.

Overlaying all of this is regulation. Measures intended to cap dark pool trading and steer flow back to lit venues have had limited impact, as activity continues to follow the path of least resistance. In practice, much of the flow has simply re-routed to SIs or other venues. The takeaway is clear; mandates alone will not resolve fragmentation. A more effective approach is probably one that balances the need for transparency with room for innovation.

Why it matters

For the buy side, fragmentation presents both opportunity and complexity. Alternative liquidity models can provide accessible, reliable, and cost-effective execution, particularly for larger or more sensitive orders. At the same time, they place greater demands on trading desks, requiring more informed decision-making, better tools, smarter routing, and a clearer understanding of how and where liquidity is accessed.

More broadly, the market faces a balancing act. Innovation is essential, but not at the expense of market integrity. Lit markets continue to play a vital role in price formation and trust, even as alternative venues offer greater flexibility and efficiency. The future is likely hybrid, supported by smart technology and thoughtful regulation, helping market participants manage complexity without losing sight of long‑term outcomes.

Prashanth Manoharan - Head of Execution Consulting

The afternoon panels are now in full swing in Amsterdam, and one session in particular caught my attention:"Measuring and controlling execution quality".

So, as you’re catching up over your second (or perhaps third) coffee of the day, here's a look ahead at what's to come.

What's going on

Electronic execution continues to grow rapidly, particularly through low‑touch workflows, and is now the dominant execution method for many clients. As trading becomes more automated and data‑driven, expectations around best execution, broker selection, and trading controls have intensified.

Against this backdrop, the focus is broadening beyond execution performance and cost alone. Increasingly, attention is turning to how broker and algorithm choices are made, the governance frameworks that sit behind those decisions, and the ability to explain and defend them with confidence as market structure and regulation continue to evolve.

Why it matters

Automation has the potential to amplify both positive and negative outcomes, making robust governance and control frameworks increasingly critical. Weak controls can heighten the risk of limit breaches, unintended behaviour, and execution outcomes that are difficult to justify after the fact.

At the same time, clients and regulators are placing greater emphasis on firms’ ability to demonstrate that broker and algorithm choices are not only effective, but fair, consistent, and auditable. As automation continues to scale, evidencing sound decision‑making is becoming just as important as delivering strong execution performance.

Michael Fidance - Head of CEEMEA Equity Markets

TradeTech Day 2 is already in motion, and I'm just about to head on stage for the "Unlocking MENA's market potential" panel, which I'll be joining as a panellist.

Before the discussion gets underway, I wanted to share a brief preview of the topics we’ll be unpacking, the key questions shaping the conversation, and why they matter for those navigating the region today.

Have a quick read before the panel kicks off!

What's going on

As asset managers enter the region or re‑engage with the emerging markets asset class, dealing desks are being asked to build expertise in some of the most complex and idiosyncratic markets globally. Volatility and liquidity, the two defining variables of any trading environment, are particularly pronounced across MENA, with conditions varying significantly by market, stock, and time of day. What is often less well understood by newer participants is that this variability extends even within the region itself, requiring desks to adjust approach and strategy to achieve their trading objectives.

For traders already active in MENA, these dynamics are well understood and have been particularly evident in recent weeks. MENA stock exchanges and the local, foreign‑investor focused broker community are pushing market structure up the curve. As a result, the opportunity to outperform on execution is becoming more tangible, and traditional, plain‑vanilla strategies such as VWAP, OTD or POV alone are no longer the only viable or safest way to trade.

Why it matters

Across the Gulf, markets continue to need new and improved sources of liquidity. Some of that will come from IPO activity, which until very recently had become a staple of the region. Outside of new deal flow, and to borrow George Orwell’s line, “all liquidity is equal, but some liquidity is more equal than others".

This is particularly true in GCC stocks, which combine a large, and at times difficult-to-access, retail component of daily turnover with an increasing presence of high‑frequency trading and its associated strategies. For a number of reasons, this evolution of activity in MENA is not particularly accretive to the needs of dedicated EM funds.

Looking beyond liquidity dynamics, the region’s growing presence in emerging market indices is becoming increasingly relevant. At the time of writing, MENA markets accounted for close to 5% (1) of aggregate EM benchmarks. While markets may appear small in isolation, the direction of travel is clear: sooner or later, the five core Gulf markets - Saudi Arabia, Dubai, Abu Dhabi, Qatar, and Kuwait - are set to represent the dominant EM weighting in this time zone. Trading and settlement rules may keep some investors away, but doing so risks notable underperformance versus peers that are actively engaged in stock‑picking across the Middle East.

1 MSCI global EM index as of March 31st

Gareth Exton - Head of Execution and Quantitative Services (EQS), EMEA

TradeTech 2026 is moving into its final stretch, but there's one more panel worth highlighting. When I saw the title “Addressable liquidity and market attractiveness: Can the consolidated tape make Europe a destination market?”,it struck me that the debate has finally moved on.

This panel is not about whether Europe should have a consolidated tape. Instead, it asks a tougher question: Now that the tape is coming, what actually changes?

What's going on

As Europe approaches the introduction of an equities and ETFs consolidated tape, the focus has shifted from principle to practice. With EuroCTP appointed, onboarding under way, and a July 2026 go‑live in view, the conversation is now firmly about implementation rather than theory.

The underlying challenge is familiar to anyone trading European equities. Liquidity is not necessarily lacking, but it is dispersed across exchanges, MTFs and off‑venue reporting, making it difficult to see the full picture, harder to analyse, and harder still to explain to global investors and issuers. The consolidated tape is intended to address this by bringing pre‑ and post‑trade data together in one place, real‑time view of trading in European shares and ETFs, with normalised timestamps, on‑venue and APA‑reported OTC activity, and European best‑price constructs alongside both composite and more granular instrument‑level views.

That’s a clear step change in data infrastructure. But at this stage, market participants do not just want to know what is in the box; they want to know whether it will actually change behaviour.

Why it matters

A consolidated tape fits neatly within the European Commission’s wider market‑structure reforms and the Savings & Investment Union agenda. The rationale is straightforward: greater transparency supports more robust price discovery, which should, over time, help deepen liquidity and strengthen Europe’s appeal as a place to trade and raise capital. At the same time, it is important to be honest about the limits. The tape can strengthen confidence in European price formation, give global investors a clearer view of the true scale of trading activity, and offer issuers better insight into how their shares trade across Europe. What it cannot do on its own is manufacture liquidity where incentives do not exist, simplify Europe’s complex market plumbing, or eliminate every competitive disadvantage relative to other regions.

Looking beyond go‑live, over a three‑ to ten‑year horizon, the more meaningful discussion is in viewing the tape not as a feed, but as infrastructure. It may become a foundation on which market participants build new analytics and strategies, fade into background plumbing as it has in other jurisdictions, or act as a catalyst for genuinely new behaviour. It may also provide policymakers with better evidence to fine‑tune incentives and market design. Seen in that light, the question of whether a consolidated tape can make Europe a destination market is really about whether it is simply the final piece of overdue transparency or the foundation on which Europe begins to function as a single, investable market.

Foosball Challenge

Check out the leaderboard from the Liquidnet booth to see who’s stacking their way to the top, one goal at a time.

Foosball Leaderboard

| Name | Score |

|---|---|

| ?????? | 1st place |

| ?????? | 2nd place |

| ?????? | 3rd place |